163 J State Conformity Chart

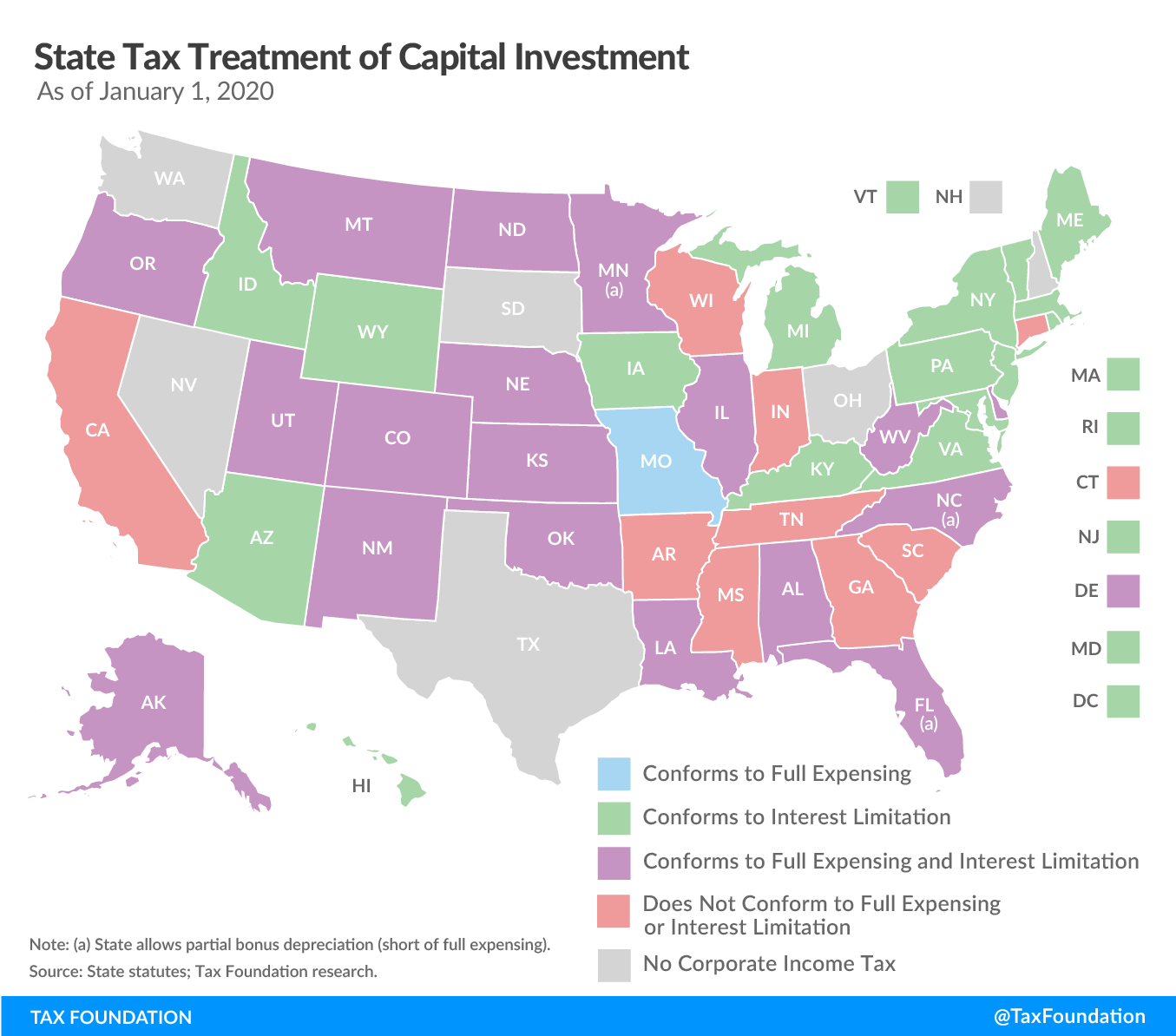

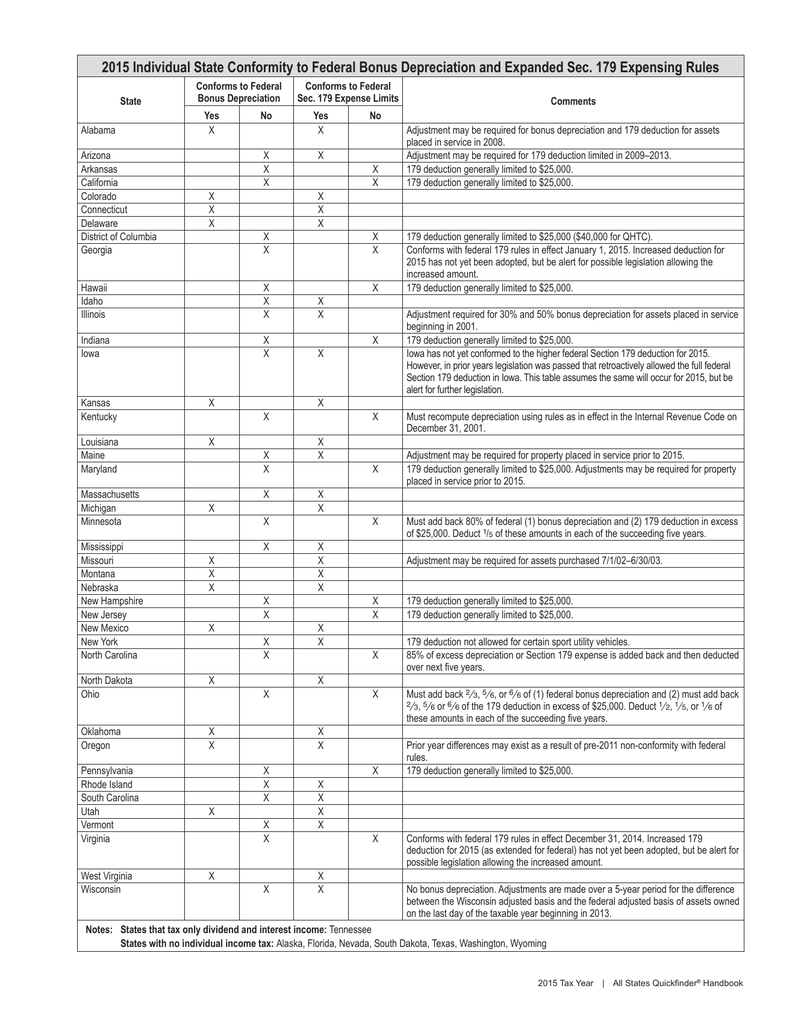

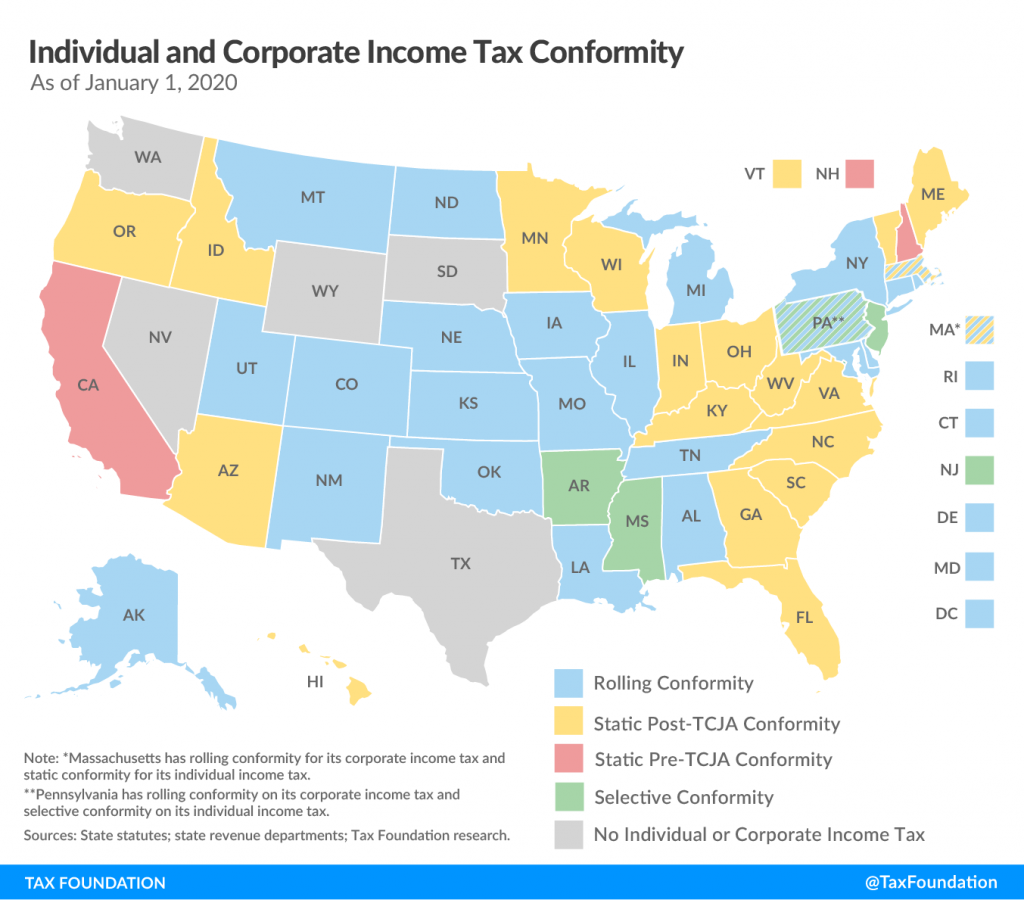

163 J State Conformity Chart - 163(j) chart identifies which states conform to cares act increase in ati to 50% as of march 27, 2020. Many states do not conform to the interest expense limitation under 163(j). 163 (j) under the tcja automatically apply to sec. Differences in federal and state law add complexity in determining how section 163 (j) applies at the state level. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but continue to use the 30 percent limit. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement. State’s taxpayers differently, depending partly on the state’s method of conformity to the internal revenue code. Section 163 (j) imposed a limit on the deductibility of business interest expense equal to the sum of business interest income, 30% of “adjusted taxable income,” and “floor. In addition, a taxpayer may elect for any tax year beginning in 2020 to use its. Decouples from the limitation under irc sec. Many states do not conform to the interest expense limitation under 163(j). Do state adjustments from sec. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement. 163 (j) under the tcja automatically apply to sec. State’s taxpayers differently, depending partly on the state’s method of conformity to the internal revenue code. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but continue to use the 30 percent limit. Recent federal tax law changes can affect each u.s. Decouples from the limitation under irc sec. Section 163 (j) imposed a limit on the deductibility of business interest expense equal to the sum of business interest income, 30% of “adjusted taxable income,” and “floor. 163 (j) provisions under the cares act? 163 (j) under the tcja automatically apply to sec. Following the enactment of the tcja, many states. In addition, a taxpayer may elect for any tax year beginning in 2020 to use its. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and. Those differences generally fall into three categories: Differences in federal and state law add complexity in determining how section 163 (j) applies at the state level. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement. Decouples from the limitation under. In addition, a taxpayer may elect for any tax year beginning in 2020 to use its. Do state adjustments from sec. 163 (j) provisions under the cares act? State’s taxpayers differently, depending partly on the state’s method of conformity to the internal revenue code. Recent federal tax law changes can affect each u.s. Many states do not conform to the interest expense limitation under 163(j). In addition to showing state carryback and carryforward allowances, the table shows the status of states’ conformity to the cares act’s suspension of the tcja limit that generally. Differences in federal and state law add complexity in determining how section 163 (j) applies at the state level. Following. Recent federal tax law changes can affect each u.s. 163 (j) under the tcja automatically apply to sec. 163(j) chart identifies which states conform to cares act increase in ati to 50% as of march 27, 2020. Those differences generally fall into three categories: Do state adjustments from sec. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but continue to use the 30 percent limit. Section 163 (j) imposed a limit on the deductibility of business interest expense equal to the sum of business interest income, 30% of “adjusted taxable income,” and “floor. Many states do not conform to the interest. Following the enactment of the tcja, many states. 163(j) chart identifies which states conform to cares act increase in ati to 50% as of march 27, 2020. State’s taxpayers differently, depending partly on the state’s method of conformity to the internal revenue code. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but. 163 (j) provisions under the cares act? These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement. In addition to showing state carryback and carryforward allowances, the table shows the status of states’ conformity to the cares act’s suspension of the. 163 (j) provisions under the cares act? 163(j) chart identifies which states conform to cares act increase in ati to 50% as of march 27, 2020. Following the enactment of the tcja, many states. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules,. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but continue to use the 30 percent limit. In addition to showing state carryback and carryforward allowances, the table shows the status of states’ conformity to the cares act’s suspension of the tcja limit that generally. Following the enactment of the tcja, many states.. Do state adjustments from sec. Differences in federal and state law add complexity in determining how section 163 (j) applies at the state level. Decouples from the limitation under irc sec. 163(j) chart identifies which states conform to cares act increase in ati to 50% as of march 27, 2020. 163 (j) under the tcja automatically apply to sec. 163 (j) provisions under the cares act? State’s taxpayers differently, depending partly on the state’s method of conformity to the internal revenue code. A taxpayer may elect not to use the 50 percent ati limit in 2019 or 2020, but continue to use the 30 percent limit. In addition to showing state carryback and carryforward allowances, the table shows the status of states’ conformity to the cares act’s suspension of the tcja limit that generally. Recent federal tax law changes can affect each u.s. These maps track specific state corporate tax law conformity to the recent federal changes made to irc § 163 (j) interest expense limitation, 80% cap rules, and qualified improvement. Following the enactment of the tcja, many states.

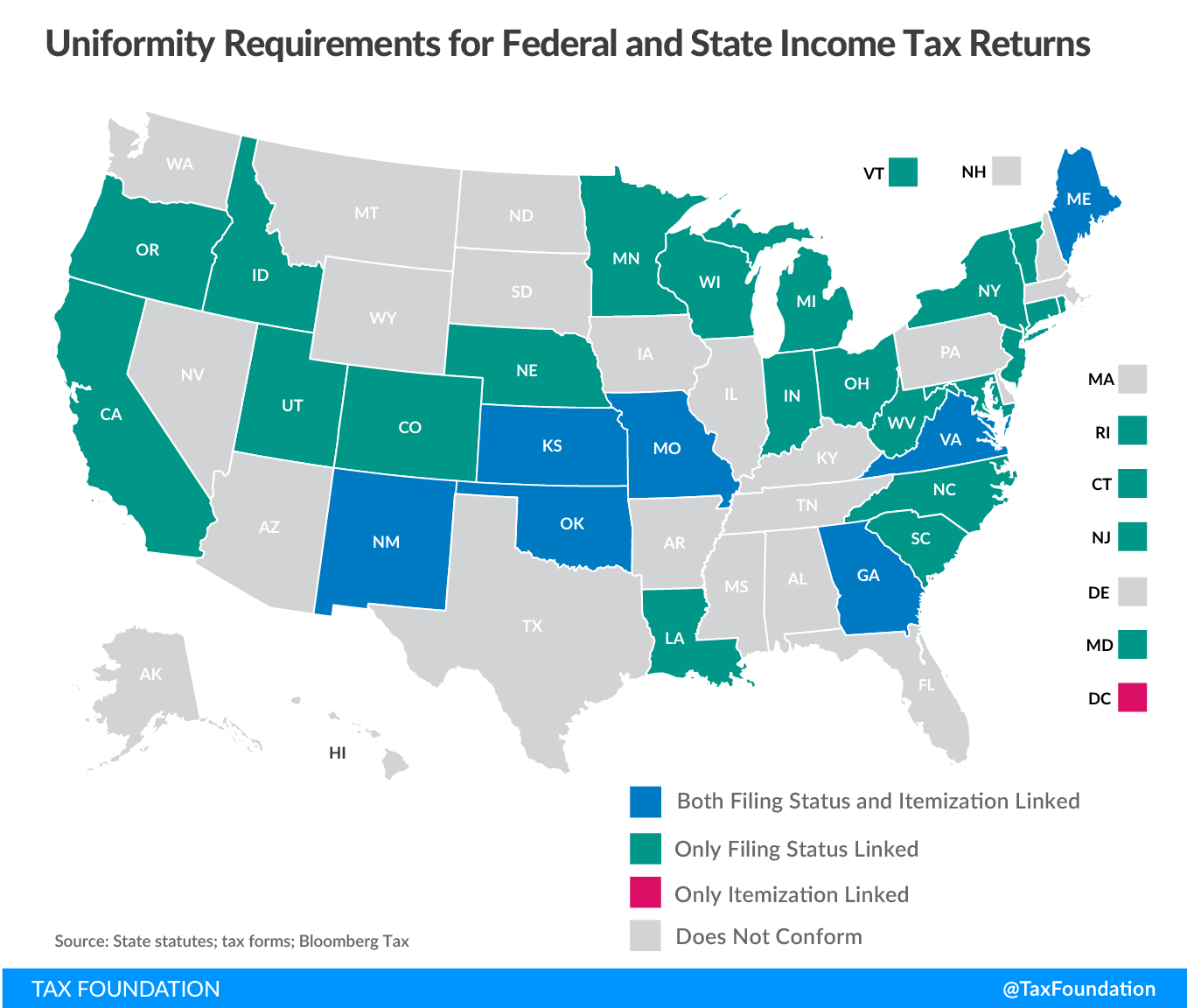

State Tax Conformity a Year After Federal Tax Reform

State Tax Conformity a Year After Federal Tax Reform

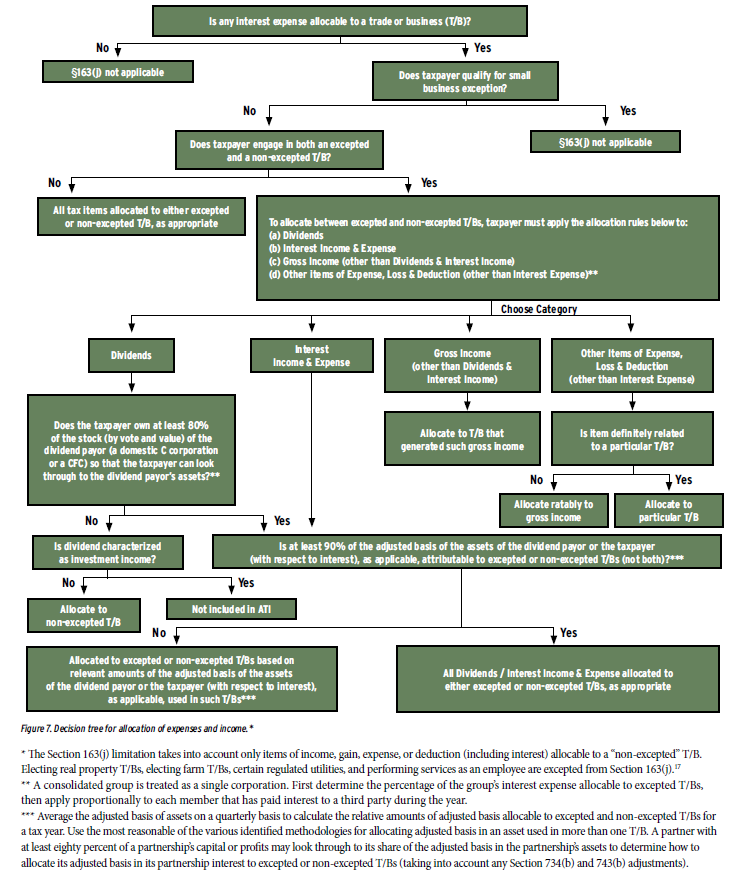

Part I The Graphic Guide to Section 163(j) Tax Executive

State Conformity to CARES Act, American Rescue Plan Tax Foundation

State Conformity to CARES Act, American Rescue Plan Tax Foundation

Federal Tax Reform Amended Sec. 163(j) Interest Expense Limitation and State Tax Conformity

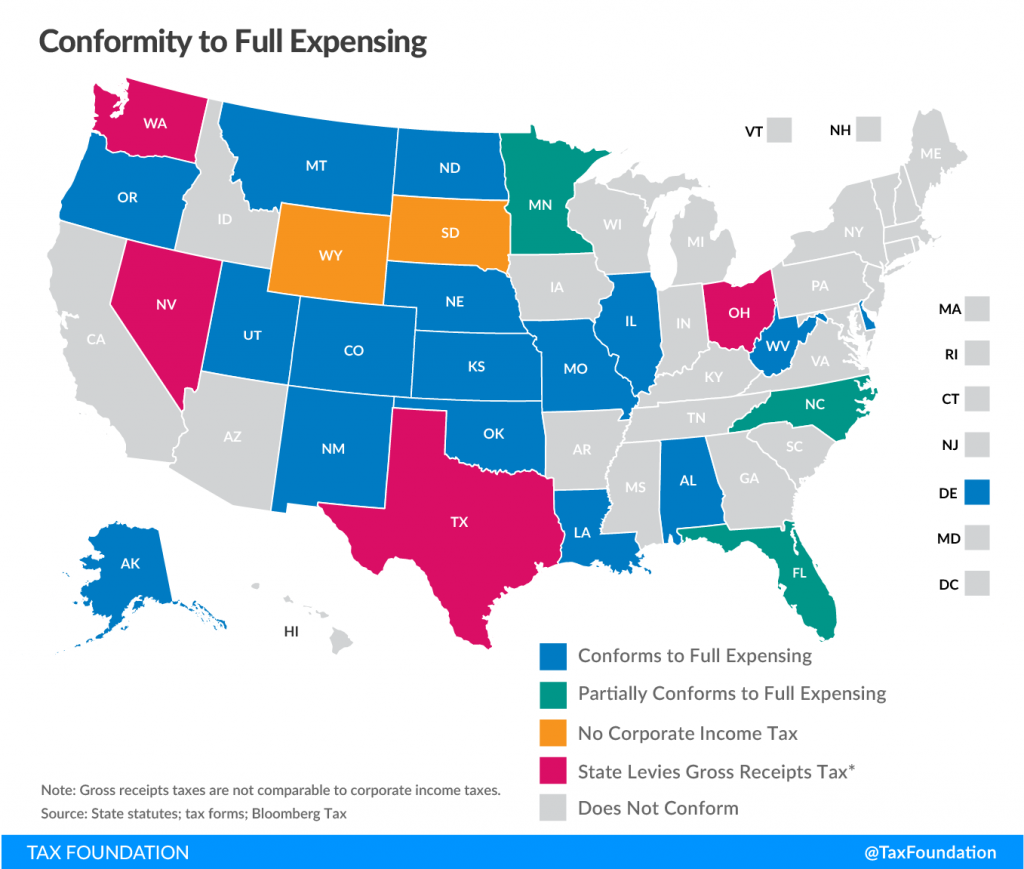

Will Arizona Lead the Way on Full Expensing This Year? Upstate Tax Professionals

163 J State Conformity Chart Portal.posgradount.edu.pe

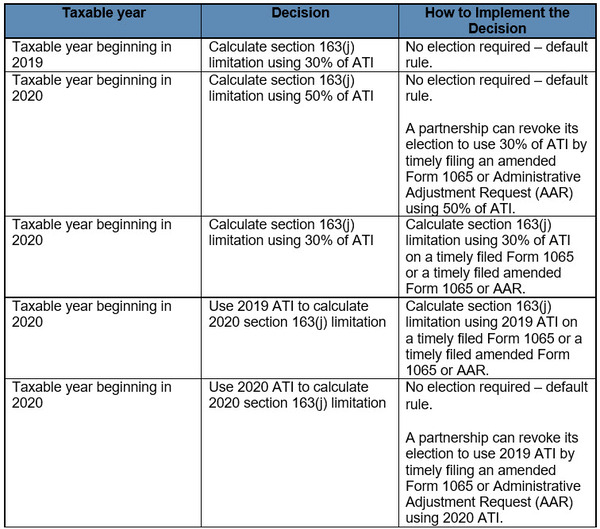

A Matter of Interest To Elect or Not to Elect the CARES Act Modifications to Section 163(j

GILTI and Other Conformity Issues Still Loom for States in 2020

Those Differences Generally Fall Into Three Categories:

Many States Do Not Conform To The Interest Expense Limitation Under 163(J).

Section 163 (J) Imposed A Limit On The Deductibility Of Business Interest Expense Equal To The Sum Of Business Interest Income, 30% Of “Adjusted Taxable Income,” And “Floor.

In Addition, A Taxpayer May Elect For Any Tax Year Beginning In 2020 To Use Its.

Related Post: